Through the almost 40 years that I have been in this escrow industry, I have been through several economic roller coaster rides that have left me dizzy and hanging on, wondering what the industry would look like when it came out of the curve.

There was no doubt that the real estate industry would survive, but in what shape or form?

The most recent one, which featured the global economic collapse between 2007 and 2008 was truly one for the history books.

And like those certain world events that we will remember forever where we were and what we were doing when they happened – the assassination of JFK, the moon landing, when the Challenger blew up, and 9/11 – the mortgage meltdown is something I will never forget because as a bystander and yet fully immersed, the events that led to the crash were easy for me to see and foretell.

Through the first few years of the 21st century we could see credit restrictions loosening up, property value increasing by leaps and bounds, and mortgage rates dropping.

A booming industry was created and the bubble got so big and so thin that it had no place to go but burst.

The watershed moment for me was encapsuled in this one event that I felt was a true indicator of things to come, one that, 12 years later, I feel I have to recount:

In 2006 a client came in to my office to sign her loan documents and she brought a friend with her.

This was a repeat customer, she and her husband had refinanced their home about a year and a half prior and they were refinancing again.

Our office was so busy we were working into the late evening hours every night and through the weekends as borrowers streamed in to sign their loan paperwork.

This couple could not come at the same time so the wife came first, with her friend.

As I signed her up my client was chatting to her friend. This utterance caught my attention, “ I just got the best looking Louis Vuitton bag, I need to show you.”

The loan package showed that they were refinancing their home to payoff 18 credit cards, ranging from a few thousand dollars to one that was about $24,000.

They were going to also cash out about $40,000, if memory serves me right, and according to the chatter, they were using the cash out portion to plan a vacation.

Why was this particular moment so memorable? It was a perfect example of what was happening at the time.

With the low interest rates and the astronomical jumps in property values, the home became the piggy bank. Loan qualifications?

We laughed and would comment that “if the borrower was breathing, they would qualify for a loan.” Whatever they stated on their loan application was their income.

Stated income was the norm. No questions asked.

Homeowners were taking advantage of this boom left and right. I had one escrow officer who had a big Countrywide Home Loan account.

She was so busy she had about 10 assistants handling the work. Countrywide loan agents were corralling everyone they could find, selling them on subprime loans with low starting adjustable rates and monthly payments that would re-set in a few months/years.

Negative amortization? Who cares? We will refinance you again when that time came, right? .

By the end of the year and the beginning of 2007, I knew that something was going to break.

This was just not sustainable.

We saw what was stated on the loan applications with their supposed monthly income and we saw their monthly payments.

How could these people afford this?

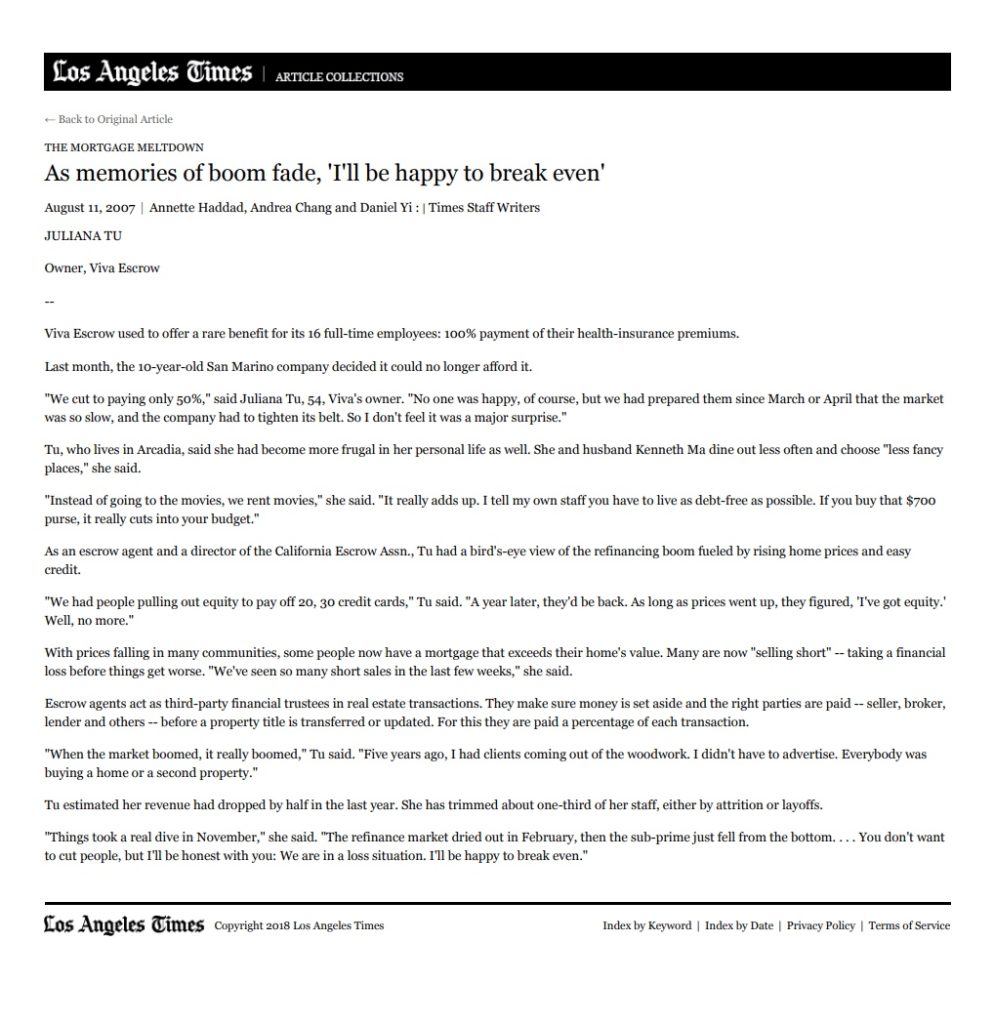

I cautioned my staff to take good care of their personal finances. “Save”, I said, “we are going to have to tighten our belts soon.” I even tried to caution the world, as my article in the Los Angeles Times mentioned.

My husband and I were coming back from Atlanta in September of 2008 when the TV screens at the airport flashed the news that Lehman Brothers was crashing.

I remember being mesmerized and right then and there I knew that the bubble had burst and the real estate industry was going for a steep dive.

Many, many people who had overreached and overspent would be in big trouble.

Afterwards it became clear that it all had to do with the subprime market and mortgage backed securities.

Ten years later and here we are. Interest rates are again low, property values have jumped.

This time around the government has been trying to correct the pendulum by swinging it from the far left to the far right.

But competition for real estate is still raging, everyone feels that the economy is doing well and unemployment is at a low.

From time to time you hear of one lender stretch out their head from the burrow to test the market with zero down loan programs, stated income loans or 1st and 2nd piggy back loans.

Shades of 2007!

I shudder when I report these attempts on my newsblog, but I know that although certain things have changed this time around (infusion of overseas money), one basic thing has not and probably never will change: Real Estate is still King.

The questions to ask now are: who gets to play and what tools are being used?

Do you have a good mortgage meltdown story to tell? Feel free to share it.

Juliana Tu, CSEO, CEO, CBSS, CEI, SASIP

Escrow Manager

Good news! “The Art of Escrow” is out! Look for it on www.amazon.com!

The Art of Escrow:

The Fight For Your American Dream and the Pursuit of Homeownership

Available now at Amazon.com

- Threats to Escrow – Part 5 – Document Fraud! - May 19, 2023

- When the Loan Got Sold and You Just Closed Escrow - April 6, 2020

- Mechanics Lien - October 7, 2019

- Are You a Foreigner and Need to Know About U.S. FIRPTA Withholding Laws? - February 20, 2019

- When the FIRPTA

Withholding Goes Wrong - February 20, 2019

Join Our FREE Viva Escrow Forums